#FactCheck -AI-Manipulated Video Falsely Claims ₹50 Crore Deal Involving Bhupen Bora

Executive Summary

A purported news clip circulating on social media claims that the Bharatiya Janata Party (BJP) purchased Bhupen Bora, a leader of the Indian National Congress, for ₹50 crore as part of a political deal in Assam. The viral clip further alleges that the transaction took place under the leadership of Assam Chief Minister Himanta Biswa Sarma and included an agreement to induct several Congress leaders into the BJP.

However, research by CyberPeace found the viral claim to be false and revealed that the original news video had been manipulated using AI and shared with misleading claims.

Claim

On February 18, 2026, a user shared the viral video on Facebook, claiming that the Assam BJP had bought a Congress leader who had lost the last three elections for ₹50 crore, and that the alleged deal led by Himanta Biswa Sarma had drawn public criticism.

Fact Check:

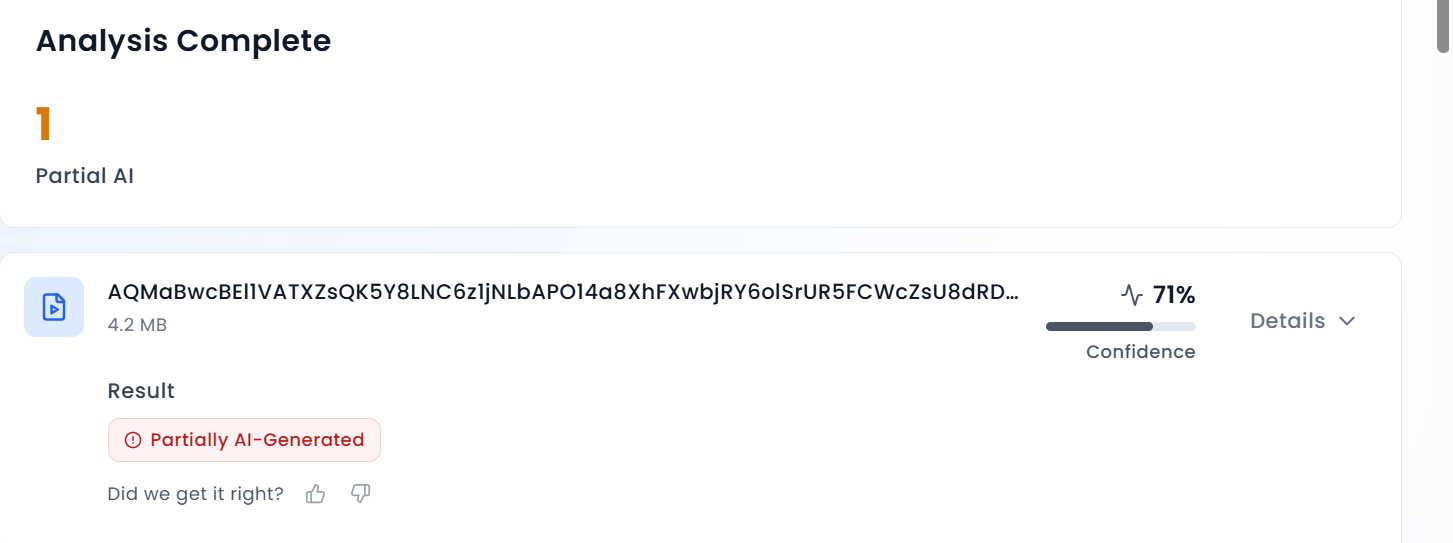

To verify the authenticity of the claim, we extracted key frames from the viral video and conducted a reverse image search using Google Lens. During the research, we found the original version of the video published on the website of Aaj Tak on February 16, 2026. In the original report, the anchor is only seen reporting on Bhupen Bora’s resignation from the party. The report does not mention any alleged financial transaction or political deal, contrary to the claims made in the viral clip.

In the next stage of the research, the viral video was analysed using the AI detection tool AURGIN AI, which identified the video as AI-generated.

Conclusion

Our research found that users had manipulated the original news broadcast using AI and shared it with misleading claims. The viral clip does not show any real financial deal between Bhupen Bora and the Assam Chief Minister.

Related Blogs

Introduction

Assisted Reproductive Technology (“ART”) refers to a diverse set of medical procedures designed to aid individuals or couples in achieving pregnancy when conventional methods are unsuccessful. This umbrella term encompasses various fertility treatments, including in vitro fertilization (IVF), intrauterine insemination (IUI), and gamete and embryo manipulation. ART procedures involve the manipulation of both male and female reproductive components to facilitate conception.

The dynamic landscape of data flows within the healthcare sector, notably in the realm of ART, demands a nuanced understanding of the complex interplay between privacy regulations and medical practices. In this context, the Information Technology (Reasonable Security Practices And Procedures And Sensitive Personal Data Or Information) Rules, 2011, play a pivotal role, designating health information as "sensitive personal data or information" and underscoring the importance of safeguarding individuals' privacy. This sensitivity is particularly pronounced in the ART sector, where an array of personal data, ranging from medical records to genetic information, is collected and processed. The recent Assisted Reproductive Technology (Regulation) Act, 2021, in conjunction with the Digital Personal Data Protection Act, 2023, establishes a framework for the regulation of ART clinics and banks, presenting a layered approach to data protection.

A note on data generated by ART

Data flows in any sector are scarcely uniform and often not easily classified under straight-jacket categories. Consequently, mapping and identifying data and its types become pivotal. It is believed that most data flows in the healthcare sector are highly sensitive and personal in nature, which may severely compromise the privacy and safety of an individual if breached. The Information Technology (Reasonable Security Practices And Procedures And Sensitive Personal Data Or Information) Rules, 2011 (“SPDI Rules”) categorizes any information pertaining to physical, physiological, mental conditions or medical records and history as “sensitive personal data or information”; this definition is broad enough to encompass any data collected by any ART facility or equipment. These include any information collected during the screening of patients, pertaining to ovulation and menstrual cycles, follicle and sperm count, ultrasound results, blood work etc. It also includes pre-implantation genetic testing on embryos to detect any genetic abnormality.

But data flows extend beyond mere medical procedures and technology. Health data also involves any medical procedures undertaken, the amount of medicine and drugs administered during any procedure, its resultant side effects, recovery etc. Any processing of the above-mentioned information, in turn, may generate more personal data points relating to an individual’s political affiliations, race, ethnicity, genetic data such as biometrics and DNA etc.; It is seen that different ethnicities and races react differently to the same/similar medication and have different propensities to genetic diseases. Further, it is to be noted that data is not only collected by professionals but also by intelligent equipment like AI which may be employed by any facility to render their service. Additionally, dissemination of information under exceptional circumstances (e.g. medical emergency) also affects how data may be classified. Considerations are further nuanced when the fundamental right to identity of a child conceived and born via ART may be in conflict with the fundamental right to privacy of a donor to remain anonymous.

Intersection of Privacy laws and ART laws:

In India, ART technology is regulated by the Assisted Reproductive Technology (Regulation) Act, 2021 (“ART Act”). With this, the Union aims to regulate and supervise assisted reproductive technology clinics and ART banks, prevent misuse and ensure safe and ethical practice of assisted reproductive technology services. When read with the Digital Personal Data Protection Act, 2023 (“DPDP Act”) and other ancillary guidelines, the two legislations provide some framework regulations for the digital privacy of health-based apps.

The ART Act establishes a National Assisted Reproductive Technology and Surrogacy Registry (“National Registry”) which acts as a central database for all clinics and banks and their nature of services. The Act also establishes a National Assisted Reproductive Technology and Surrogacy Board (“National Board”) under the Surrogacy Act to monitor the implementation of the act and advise the central government on policy matters. It also supervises the functioning of the National Registry, liaises with State Boards and curates a code of conduct for professionals working in ART clinics and banks. Under the DPDP Act, these bodies (i.e. National Board, State Board, ART clinics and banks) are most likely classified as data fiduciaries (primarily clinics and banks), data processors (these may include National Board and State boards) or an amalgamation of both (these include any appropriate authority established under the ART Act for investigation of complaints, suspend or cancellation of registration of clinics etc.) depending on the nature of work undertaken by them. If so classified, then the duties and liabilities of data fiduciaries and processors would necessarily apply to these bodies. As a result, all bodies would necessarily have to adopt Privacy Enhancing Technologies (PETs) and other organizational measures to ensure compliance with privacy laws in place. This may be considered one of the most critical considerations of any ART facility since any data collected by them would be sensitive personal data pertaining to health, regulated by the Information Technology (Reasonable Security Practices And Procedures And Sensitive Personal Data Or Information) Rules, 2011 (“SPDI Rules 2011”). These rules provide for how sensitive personal data or information are to be collected, handled and processed by anyone.

The ART Act independently also provides for the duties of ART clinics and banks in the country. ART clinics and banks are required to inform the commissioning couple/woman of all procedures undertaken and all costs, risks, advantages, and side effects of their selected procedure. It mandatorily ensures that all information collected by such clinics and banks to not informed to anyone except the database established by the National Registry or in cases of medical emergency or on order of court. Data collected by clinics and banks (these include details on donor oocytes, sperm or embryos used or unused) are required to be detailed and must be submitted to the National Registry online. ART banks are also required to collect personal information of donors including name, Aadhar number, address and any other details. By mandating online submission, the ART Act is harmonized with the DPDP Act, which regulates all digital personal data and emphasises free, informed consent.

Conclusion

With the increase in active opt-ins for ART, data privacy becomes a vital consideration for all healthcare facilities and professionals. Safeguard measures are not only required on a corporate level but also on a governmental level. It is to be noted that in the 262 Session of the Rajya Sabha, the Ministry of Electronics and Information Technology reported 165 data breach incidents involving citizen data from January 2018 to October 2023 from the Central Identities Data Repository despite publicly denying. This discovery puts into question the safety and integrity of data that may be submitted to the National Registry database, especially given the type of data (both personal and sensitive information) it aims to collate. At present the ART Act is well supported by the DPDP Act. However, further judicial and legislative deliberations are required to effectively regulate and balance the interests of all stakeholders.

References

- The Information Technology (Reasonable Security Practices And Procedures And Sensitive Personal Data Or Information) Rules, 2011

- Caring for Intimate Data in Fertility Technologies https://dl.acm.org/doi/pdf/10.1145/3411764.3445132

- Digital Personal Data Protection Act, 2023

- https://www.wolterskluwer.com/en/expert-insights/pharmacogenomics-and-race-can-heritage-affect-drug-disposition

.webp)

Executive Summary:

A widely used news on social media is that a 3D model of Chanakya, supposedly made by Magadha DS University matches with MS Dhoni. However, fact-checking reveals that it is a 3D model of MS Dhoni not Chanakya. This MS Dhoni-3D model was created by artist Ankur Khatri and Magadha DS University does not appear to exist in the World. Khatri uploaded the model on ArtStation, calling it an MS Dhoni similarity study.

Claims:

The image being shared is claimed to be a 3D rendering of the ancient philosopher Chanakya created by Magadha DS University. However, people are noticing a striking similarity to the Indian cricketer MS Dhoni in the image.

Fact Check:

After receiving the post, we ran a reverse image search on the image. We landed on a Portfolio of a freelance character model named Ankur Khatri. We found the viral image over there and he gave a headline to the work as “MS Dhoni likeness study”. We also found some other character models in his portfolio.

Subsequently, we searched for the mentioned University which was named as Magadha DS University. But found no University with the same name, instead the name is Magadh University and it is located in Bodhgaya, Bihar. We searched the internet for any model, made by Magadh University but found nothing. The next step was to conduct an analysis on the Freelance Character artist profile, where we found that he has a dedicated Instagram channel where he posted a detailed video of his creative process that resulted in the MS Dhoni character model.

We concluded that the viral image is not a reconstruction of Indian philosopher Chanakya but a reconstruction of Cricketer MS Dhoni created by an artist named Ankur Khatri, not any University named Magadha DS.

Conclusion:

The viral claim that the 3D model is a recreation of the ancient philosopher Chanakya by a university called Magadha DS University is False and Misleading. In reality, the model is a digital artwork of former Indian cricket captain MS Dhoni, created by artist Ankur Khatri. There is no evidence of a Magadha DS University existence. There is a university named Magadh University in Bodh Gaya, Bihar despite its similar name, we found no evidence in the model's creation. Therefore, the claim is debunked, and the image is confirmed to be a depiction of MS Dhoni, not Chanakya.

Introduction

With the increasing frequency and severity of cyber-attacks on critical sectors, the government of India has formulated the National Cyber Security Reference Framework (NCRF) 2023, aimed to address cybersecurity concerns in India. In today’s digital age, the security of critical sectors is paramount due to the ever-evolving landscape of cyber threats. Cybersecurity measures are crucial for protecting essential sectors such as banking, energy, healthcare, telecommunications, transportation, strategic enterprises, and government enterprises. This is an essential step towards safeguarding these critical sectors and preparing for the challenges they face in the face of cyber threats. Protecting critical sectors from cyber threats is an urgent priority that requires the development of robust cybersecurity practices and the implementation of effective measures to mitigate risks.

Overview of the National Cyber Security Policy 2013

The National Cyber Security Policy of 2013 was the first attempt to address cybersecurity concerns in India. However, it had several drawbacks that limited its effectiveness in mitigating cyber risks in the contemporary digital age. The policy’s outdated guidelines, insufficient prevention and response measures, and lack of legal implications hindered its ability to protect critical sectors adequately. Moreover, the policy should have kept up with the rapidly evolving cyber threat landscape and emerging technologies, leaving organisations vulnerable to new cyber-attacks. The 2013 policy failed to address the evolving nature of cyber threats, leaving organisations needing updated guidelines to combat new and sophisticated attacks.

As a result, an updated and more comprehensive policy, the National Cyber Security Reference Framework 2023, was necessary to address emerging challenges and provide strategic guidance for protecting critical sectors against cyber threats.

Highlights of NCRF 2023

Strategic Guidance: NCRF 2023 has been developed to provide organisations with strategic guidance to address their cybersecurity concerns in a structured manner.

Common but Differentiated Responsibility (CBDR): The policy is based on a CBDR approach, recognising that different organisations have varying levels of cybersecurity needs and responsibilities.

Update of National Cyber Security Policy 2013: NCRF supersedes the National Cyber Security Policy 2013, which was due for an update to align with the evolving cyber threat landscape and emerging challenges.

Different from CERT-In Directives: NCRF is distinct from the directives issued by the Indian Computer Emergency Response Team (CERT-In) published in April 2023. It provides a comprehensive framework rather than specific directives for reporting cyber incidents.

Combination of robust strategies: National Cyber Security Reference Framework 2023 will provide strategic guidance, a revised structure, and a proactive approach to cybersecurity, enabling organisations to tackle the growing cyberattacks in India better and safeguard critical sectors. Rising incidents of malware attacks on critical sectors

In recent years, there has been a significant increase in malware attacks targeting critical sectors. These sectors, including banking, energy, healthcare, telecommunications, transportation, strategic enterprises, and government enterprises, play a crucial role in the functioning of economies and the well-being of societies. The escalating incidents of malware attacks on these sectors have raised concerns about the security and resilience of critical infrastructure.

Banking: The banking sector handles sensitive financial data and is a prime target for cybercriminals due to the potential for financial fraud and theft.

Energy: The energy sector, including power grids and oil companies, is critical for the functioning of economies, and disruptions can have severe consequences for national security and public safety.

Healthcare: The healthcare sector holds valuable patient data, and cyber-attacks can compromise patient privacy and disrupt healthcare services. Malware attacks on healthcare organisations can result in the theft of patient records, ransomware incidents that cripple healthcare operations, and compromise medical devices.

Telecommunications: Telecommunications infrastructure is vital for reliable communication, and attacks targeting this sector can lead to communication disruptions and compromise the privacy of transmitted data. The interconnectedness of telecommunications networks globally presents opportunities for cybercriminals to launch large-scale attacks, such as Distributed Denial-of-Service (DDoS) attacks.

Transportation: Malware attacks on transportation systems can lead to service disruptions, compromise control systems, and pose safety risks.

Strategic Enterprises: Strategic enterprises, including defence, aerospace, intelligence agencies, and other sectors vital to national security, face sophisticated malware attacks with potentially severe consequences. Cyber adversaries target these enterprises to gain unauthorised access to classified information, compromise critical infrastructure, or sabotage national security operations.

Government Enterprises: Government organisations hold a vast amount of sensitive data and provide essential services to citizens, making them targets for data breaches and attacks that can disrupt critical services.

Conclusion

The sectors of banking, energy, healthcare, telecommunications, transportation, strategic enterprises, and government enterprises face unique vulnerabilities and challenges in the face of cyber-attacks. By recognising the significance of safeguarding these sectors, we can emphasise the need for proactive cybersecurity measures and collaborative efforts between public and private entities. Strengthening regulatory frameworks, sharing threat intelligence, and adopting best practices are essential to ensure our critical infrastructure’s resilience and security. Through these concerted efforts, we can create a safer digital environment for these sectors, protecting vital services and preserving the integrity of our economy and society. The rising incidents of malware attacks on critical sectors emphasise the urgent need for updated cybersecurity policy, enhanced cybersecurity measures, a collaboration between public and private entities, and the development of proactive defence strategies. National Cyber Security Reference Framework 2023 will help in addressing the evolving cyber threat landscape, protect critical sectors, fill the gaps in sector-specific best practices, promote collaboration, establish a regulatory framework, and address the challenges posed by emerging technologies. By providing strategic guidance, this framework will enhance organisations’ cybersecurity posture and ensure the protection of critical infrastructure in an increasingly digitised world.