#FactCheck: Viral Deepfake Video of Modi, Shah, Jaishankar Apologize for Operation Sindoor Blunder

Executive Summary:

Recently, we came upon some AI-generated deep fake videos that have gone viral on social media, purporting to show Indian political figures Prime Minister Narendra Modi, Home Minister Amit Shah, and External Affairs Minister Dr. S. Jaishankar apologizing in public for initiating "Operation Sindoor." The videos are fake and use artificial intelligence tools to mimic the leaders' voices and appearances, as concluded by our research. The purpose of this report is to provide a clear understanding of the facts and to reveal the truth behind these viral videos.

Claim:

Multiple videos circulating on social media claim to show Prime Minister Narendra Modi, Central Home Minister Amit Shah, and External Affairs Minister Dr. S. Jaishankar publicly apologised for launching "Operation Sindoor." The videos, which are being circulated to suggest a political and diplomatic failure, feature the leaders speaking passionately and expressing regret over the operation.

Fact Check:

Our research revealed that the widely shared videos were deepfakes made with artificial intelligence tools. Following the 22 April 2025 Pahalgam terror attack, after “Operation Sindoor”, which was held by the Indian Armed Forces, this video emerged, intending to spread false propaganda and misinformation.

Finding important frames and visual clues from the videos that seemed suspicious, such as strange lip movements, misaligned audio, and facial distortions, was the first step in the fact-checking process. By putting audio samples and video frames in Hive AI Content Moderation, a program for detecting AI-generated content. After examining audio, facial, and visual cues, Hive's deepfake detection system verified that all three of the videos were artificial intelligence (AI) produced.

Below are three Hive Moderator result screenshots that clearly flag the videos as synthetic content, confirming that none of them are authentic or released by any official government source.

Conclusion:

The artificial intelligence-generated videos that claim Prime Minister Narendra Modi, Home Minister Amit Shah, and External Affairs Minister Dr. S. Jaishankar apologized for the start of "Operation Sindoor" are completely untrue. A purposeful disinformation campaign to mislead the public and incite political unrest includes these deepfake videos. No such apology has been made by the Indian government, and the operation in question does not exist in any official or verified capacity. The public must exercise caution, avoid disseminating videos that have not been verified, and rely on reliable fact-checking websites. Such disinformation can seriously affect national discourse and security in addition to eroding public trust.

- Claim: India's top executives apologize publicly for Operation Sindoor blunder.

- Claimed On: Social Media

- Fact Check: AI Misleads

Related Blogs

Executive Summary

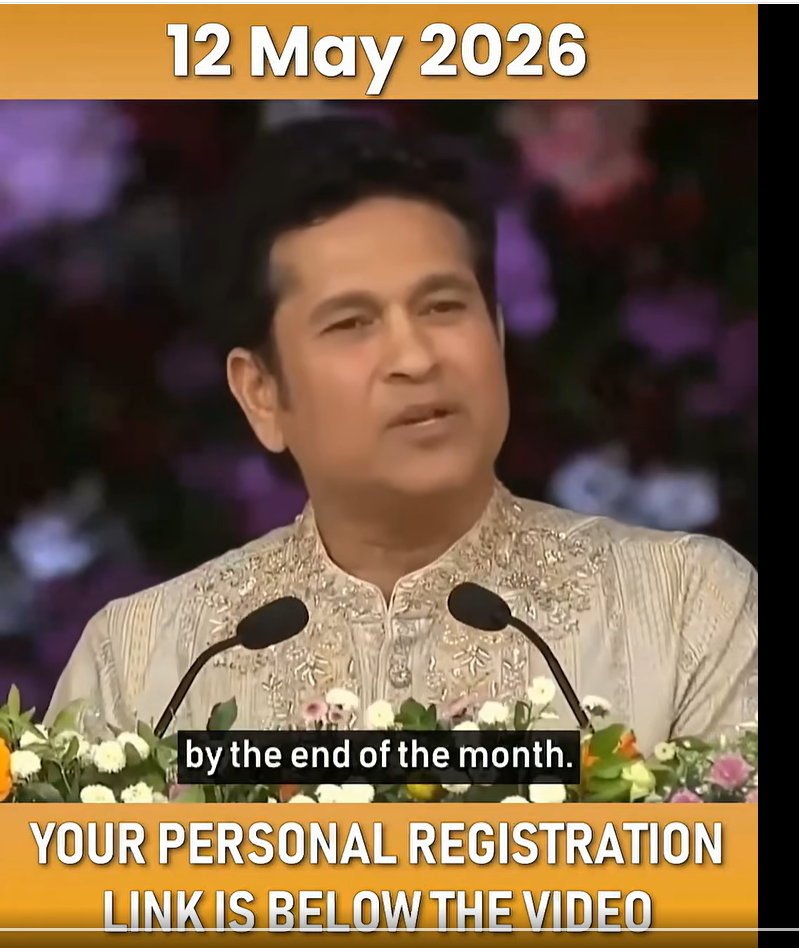

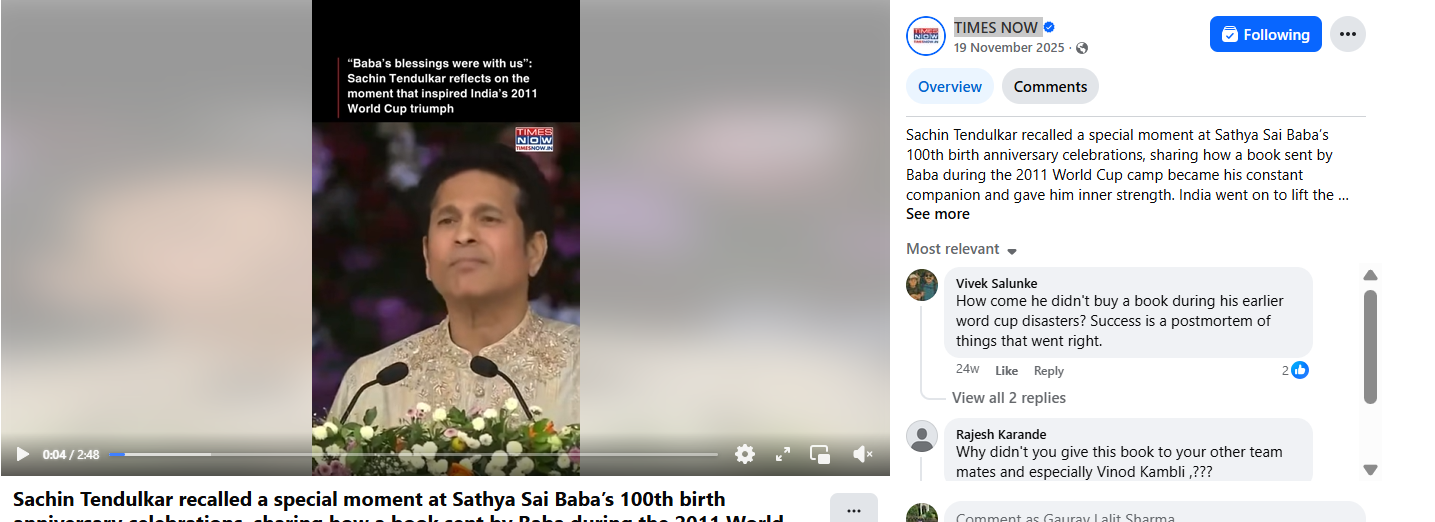

A video featuring former Indian cricketer Sachin Tendulkar is being widely circulated on social media with the date “12-5-2026” displayed on the screen. In the viral clip, Tendulkar appears to promote an investment scheme, allegedly saying that people investing in the scheme today could earn Rs 80 lakh by the end of the day. Throughout the video, he is seen speaking about investment opportunities and financial returns. However, research conducted by CyberPeace Research Wing found that the video is AI-generated and misleading. The original footage was actually from an event marking the centenary celebrations of Sri Sathya Sai Baba.

Claim

A Facebook user shared the viral video on May 12, 2026, claiming that Sachin Tendulkar was endorsing a high-return investment scheme. The post quickly gained traction on social media platforms.

Fact Check

To verify the claim, we searched the internet using relevant keywords but found no credible media reports suggesting that Tendulkar had endorsed any such investment scheme. As part of our research, we extracted key frames from the viral clip and conducted a reverse image search. During the search, we found the original video uploaded on November 19, 2025, on the YouTube channel of IANS. According to the video description, Tendulkar was attending an event organized to mark the centenary year celebrations of Sri Sathya Sai Baba.

We further found a similar version of the same video uploaded on November 19, 2025, on the official Facebook page of Times Now, confirming that the footage was unrelated to any investment or financial scheme.

Conclusion

Our research found that the viral video has been manipulated using AI-generated audio or editing techniques to falsely portray Sachin Tendulkar promoting an investment scheme. The original video was from a public event related to Sri Sathya Sai Baba’s centenary celebrations and had no connection to any financial investment platform.

.webp)

Executive Summary:

A post on X (formerly Twitter) has gained widespread attention, featuring an image inaccurately asserting that Houthi rebels attacked a power plant in Ashkelon, Israel. This misleading content has circulated widely amid escalating geopolitical tensions. However, investigation shows that the footage actually originates from a prior incident in Saudi Arabia. This situation underscores the significant dangers posed by misinformation during conflicts and highlights the importance of verifying sources before sharing information.

Claims:

The viral video claims to show Houthi rebels attacking Israel's Ashkelon power plant as part of recent escalations in the Middle East conflict.

Fact Check:

Upon receiving the viral posts, we conducted a Google Lens search on the keyframes of the video. The search reveals that the video circulating online does not refer to an attack on the Ashkelon power plant in Israel. Instead, it depicts a 2022 drone strike on a Saudi Aramco facility in Abqaiq. There are no credible reports of Houthi rebels targeting Ashkelon, as their activities are largely confined to Yemen and Saudi Arabia.

This incident highlights the risks associated with misinformation during sensitive geopolitical events. Before sharing viral posts, take a brief moment to verify the facts. Misinformation spreads quickly and it’s far better to rely on trusted fact-checking sources.

Conclusion:

The assertion that Houthi rebels targeted the Ashkelon power plant in Israel is incorrect. The viral video in question has been misrepresented and actually shows a 2022 incident in Saudi Arabia. This underscores the importance of being cautious when sharing unverified media. Before sharing viral posts, take a moment to verify the facts. Misinformation spreads quickly, and it is far better to rely on trusted fact-checking sources.

- Claim: The video shows massive fire at Israel's Ashkelon power plant

- Claimed On:Instagram and X (Formerly Known As Twitter)

- Fact Check: False and Misleading

Overview:

The rapid digitization of educational institutions in India has created both opportunities and challenges. While technology has improved access to education and administrative efficiency, it has also exposed institutions to significant cyber threats. This report, published by CyberPeace, examines the types, causes, impacts, and preventive measures related to cyber risks in Indian educational institutions. It highlights global best practices, national strategies, and actionable recommendations to mitigate these threats.

Significance of the Study:

The pandemic-induced shift to online learning, combined with limited cybersecurity budgets, has made educational institutions prime targets for cyberattacks. These threats compromise sensitive student, faculty, and institutional data, leading to operational disruptions, financial losses, and reputational damage. Globally, educational institutions face similar challenges, emphasizing the need for universal and localized responses.

Threat Faced by Education Institutions:

Based on the insights from the CyberPeace’s report titled 'Exploring Cyber Threats and Digital Risks in Indian Educational Institutions', this concise blog provides a comprehensive overview of cybersecurity threats and risks faced by educational institutions, along with essential details to address these challenges.

🎣 Phishing: Phishing is a social engineering tactic where cyber criminals impersonate trusted sources to steal sensitive information, such as login credentials and financial details. It often involves deceptive emails or messages that lead to counterfeit websites, pressuring victims to provide information quickly. Variants include spear phishing, smishing, and vishing.

💰 Ransomware: Ransomware is malware that locks users out of their systems or data until a ransom is paid. It spreads through phishing emails, malvertising, and exploiting vulnerabilities, causing downtime, data leaks, and theft. Ransom demands can range from hundreds to hundreds of thousands of dollars.

🌐 Distributed Denial of Service (DDoS): DDoS attacks overwhelm servers, denying users access to websites and disrupting daily operations, which can hinder students and teachers from accessing learning resources or submitting assignments. These attacks are relatively easy to execute, especially against poorly protected networks, and can be carried out by amateur cybercriminals, including students or staff, seeking to cause disruptions for various reasons

🕵️ Cyber Espionage: Higher education institutions, particularly research-focused universities, are vulnerable to spyware, insider threats, and cyber espionage. Spyware is unauthorized software that collects sensitive information or damages devices. Insider threats arise from negligent or malicious individuals, such as staff or vendors, who misuse their access to steal intellectual property or cause data leaks..

🔒 Data Theft: Data theft is a major threat to educational institutions, which store valuable personal and research information. Cybercriminals may sell this data or use it for extortion, while stealing university research can provide unfair competitive advantages. These attacks can go undetected for long periods, as seen in the University of California, Berkeley breach, where hackers allegedly stole 160,000 medical records over several months.

🛠️ SQL Injection: SQL injection (SQLI) is an attack that uses malicious code to manipulate backend databases, granting unauthorized access to sensitive information like customer details. Successful SQLI attacks can result in data deletion, unauthorized viewing of user lists, or administrative access to the database.

🔍Eavesdropping attack: An eavesdropping breach, or sniffing, is a network attack where cybercriminals steal information from unsecured transmissions between devices. These attacks are hard to detect since they don't cause abnormal data activity. Attackers often use network monitors, like sniffers, to intercept data during transmission.

🤖 AI-Powered Attacks: AI enhances cyber attacks like identity theft, password cracking, and denial-of-service attacks, making them more powerful, efficient, and automated. It can be used to inflict harm, steal information, cause emotional distress, disrupt organizations, and even threaten national security by shutting down services or cutting power to entire regions

Insights from Project eKawach

The CyberPeace Research Wing, in collaboration with SAKEC CyberPeace Center of Excellence (CCoE) and Autobot Infosec Private Limited, conducted a study simulating educational institutions' networks to gather intelligence on cyber threats. As part of the e-Kawach project, a nationwide initiative to strengthen cybersecurity, threat intelligence sensors were deployed to monitor internet traffic and analyze real-time cyber attacks from July 2023 to April 2024, revealing critical insights into the evolving cyber threat landscape.

Cyber Attack Trends

Between July 2023 and April 2024, the e-Kawach network recorded 217,886 cyberattacks from IP addresses worldwide, with a significant portion originating from countries including the United States, China, Germany, South Korea, Brazil, Netherlands, Russia, France, Vietnam, India, Singapore, and Hong Kong. However, attributing these attacks to specific nations or actors is complex, as threat actors often use techniques like exploiting resources from other countries, or employing VPNs and proxies to obscure their true locations, making it difficult to pinpoint the real origin of the attacks.

Brute Force Attack:

The analysis uncovered an extensive use of automated tools in brute force attacks, with 8,337 unique usernames and 54,784 unique passwords identified. Among these, the most frequently targeted username was “root,” which accounted for over 200,000 attempts. Other commonly targeted usernames included: "admin", "test", "user", "oracle", "ubuntu", "guest", "ftpuser", "pi", "support"

Similarly, the study identified several weak passwords commonly targeted by attackers. “123456” was attempted over 3,500 times, followed by “password” with over 2,500 attempts. Other frequently targeted passwords included: "1234", "12345", "12345678", "admin", "123", "root", "test", "raspberry", "admin123", "123456789"

Insights from Threat Landscape Analysis

Research done by the USI - CyberPeace Centre of Excellence (CCoE) and Resecurity has uncovered several breached databases belonging to public, private, and government universities in India, highlighting significant cybersecurity threats in the education sector. The research aims to identify and mitigate cybersecurity risks without harming individuals or assigning blame, based on data available at the time, which may evolve with new information. Institutions were assigned risk ratings that descend from A to F, with most falling under a D rating, indicating numerous security vulnerabilities. Institutions rated D or F are 5.4 times more likely to experience data breaches compared to those rated A or B. Immediate action is recommended to address the identified risks.

Risk Findings :

The risk findings for the institutions are summarized through a pie chart, highlighting factors such as data breaches, dark web activity, botnet activity, and phishing/domain squatting. Data breaches and botnet activity are significantly higher compared to dark web leakages and phishing/domain squatting. The findings show 393,518 instances of data breaches, 339,442 instances of botnet activity, 7,926 instances related to the dark web and phishing & domain activity - 6711.

Key Indicators: Multiple instances of data breaches containing credentials (email/passwords) in plain text.

- Botnet activity indicating network hosts compromised by malware.

- Credentials from third-party government and non-governmental websites linked to official institutional emails

- Details of software applications, drivers installed on compromised hosts.

- Sensitive cookie data exfiltrated from various browsers.

- IP addresses of compromised systems.

- Login credentials for different Android applications.

Below is the sample detail of one of the top educational institutions that provides the insights about the higher rate of data breaches, botnet activity, dark web activities and phishing & domain squatting.

Risk Detection:

It indicates the number of data breaches, network hygiene, dark web activities, botnet activities, cloud security, phishing & domain squatting, media monitoring and miscellaneous risks. In the below example, we are able to see the highest number of data breaches and botnet activities in the sample particular domain.

Risk Changes:

Risk by Categories:

Risk is categorized with factors such as high, medium and low, the risk is at high level for data breaches and botnet activities.

Challenges Faced by Educational Institutions

Educational institutions face cyberattack risks, the challenges leading to cyberattack incidents in educational institutions are as follows:

🔒 Lack of a Security Framework: A key challenge in cybersecurity for educational institutions is the lack of a dedicated framework for higher education. Existing frameworks like ISO 27001, NIST, COBIT, and ITIL are designed for commercial organizations and are often difficult and costly to implement. Consequently, many educational institutions in India do not have a clearly defined cybersecurity framework.

🔑 Diverse User Accounts: Educational institutions manage numerous accounts for staff, students, alumni, and third-party contractors, with high user turnover. The continuous influx of new users makes maintaining account security a challenge, requiring effective systems and comprehensive security training for all users.

📚 Limited Awareness: Cybersecurity awareness among students, parents, teachers, and staff in educational institutions is limited due to the recent and rapid integration of technology. The surge in tech use, accelerated by the pandemic, has outpaced stakeholders' ability to address cybersecurity issues, leaving them unprepared to manage or train others on these challenges.

📱 Increased Use of Personal/Shared Devices: The growing reliance on unvetted personal/Shared devices for academic and administrative activities amplifies security risks.

💬 Lack of Incident Reporting: Educational institutions often neglect reporting cyber incidents, increasing vulnerability to future attacks. It is essential to report all cases, from minor to severe, to strengthen cybersecurity and institutional resilience.

Impact of Cybersecurity Attacks on Educational Institutions

Cybersecurity attacks on educational institutions lead to learning disruptions, financial losses, and data breaches. They also harm the institution's reputation and pose security risks to students. The following are the impacts of cybersecurity attacks on educational institutions:

📚Impact on the Learning Process: A report by the US Government Accountability Office (GAO) found that cyberattacks on school districts resulted in learning losses ranging from three days to three weeks, with recovery times taking between two to nine months.

💸Financial Loss: US schools reported financial losses ranging from $50,000 to $1 million due to expenses like hardware replacement and cybersecurity upgrades, with recovery taking an average of 2 to 9 months.

🔒Data Security Breaches: Cyberattacks exposed sensitive data, including grades, social security numbers, and bullying reports. Accidental breaches were often caused by staff, accounting for 21 out of 25 cases, while intentional breaches by students, comprising 27 out of 52 cases, frequently involved tampering with grades.

⚠️Data Security Breach: Cyberattacks on schools result in breaches of personal information, including grades and social security numbers, causing emotional, physical, and financial harm. These breaches can be intentional or accidental, with a US study showing staff responsible for most accidental breaches (21 out of 25) and students primarily behind intentional breaches (27 out of 52) to change grades.

🏫Impact on Institutional Reputation: Cyberattacks damaged the reputation of educational institutions, eroding trust among students, staff, and families. Negative media coverage and scrutiny impacted staff retention, student admissions, and overall credibility.

🛡️ Impact on Student Safety: Cyberattacks compromised student safety and privacy. For example, breaches like live-streaming school CCTV footage caused severe distress, negatively impacting students' sense of security and mental well-being.

CyberPeace Advisory:

CyberPeace emphasizes the importance of vigilance and proactive measures to address cybersecurity risks:

- Develop effective incident response plans: Establish a clear and structured plan to quickly identify, respond to, and recover from cyber threats. Ensure that staff are well-trained and know their roles during an attack to minimize disruption and prevent further damage.

- Implement access controls with role-based permissions: Restrict access to sensitive information based on individual roles within the institution. This ensures that only authorized personnel can access certain data, reducing the risk of unauthorized access or data breaches.

- Regularly update software and conduct cybersecurity training: Keep all software and systems up-to-date with the latest security patches to close vulnerabilities. Provide ongoing cybersecurity awareness training for students and staff to equip them with the knowledge to prevent attacks, such as phishing.

- Ensure regular and secure backups of critical data: Perform regular backups of essential data and store them securely in case of cyber incidents like ransomware. This ensures that, if data is compromised, it can be restored quickly, minimizing downtime.

- Adopt multi-factor authentication (MFA): Enforce Multi-Factor Authentication(MFA) for accessing sensitive systems or information to strengthen security. MFA adds an extra layer of protection by requiring users to verify their identity through more than one method, such as a password and a one-time code.

- Deploy anti-malware tools: Use advanced anti-malware software to detect, block, and remove malicious programs. This helps protect institutional systems from viruses, ransomware, and other forms of malware that can compromise data security.

- Monitor networks using intrusion detection systems (IDS): Implement IDS to monitor network traffic and detect suspicious activity. By identifying threats in real time, institutions can respond quickly to prevent breaches and minimize potential damage.

- Conduct penetration testing: Regularly conduct penetration testing to simulate cyberattacks and assess the security of institutional networks. This proactive approach helps identify vulnerabilities before they can be exploited by actual attackers.

- Collaborate with cybersecurity firms: Partner with cybersecurity experts to benefit from specialized knowledge and advanced security solutions. Collaboration provides access to the latest technologies, threat intelligence, and best practices to enhance the institution's overall cybersecurity posture.

- Share best practices across institutions: Create forums for collaboration among educational institutions to exchange knowledge and strategies for cybersecurity. Sharing successful practices helps build a collective defense against common threats and improves security across the education sector.

Conclusion:

The increasing cyber threats to Indian educational institutions demand immediate attention and action. With vulnerabilities like data breaches, botnet activities, and outdated infrastructure, institutions must prioritize effective cybersecurity measures. By adopting proactive strategies such as regular software updates, multi-factor authentication, and incident response plans, educational institutions can mitigate risks and safeguard sensitive data. Collaborative efforts, awareness, and investment in cybersecurity will be essential to creating a secure digital environment for academia.